২০২৫ সালে পরিবারের জন্য সেরা জীবন বীমা পরিকল্পনা

একটি নিরাপদ ভবিষ্যৎ গড়ে তুলতে পরিবারকে সুরক্ষিত রাখা খুবই গুরুত্বপূর্ণ। জীবন বীমা সেই নিরাপত্তার অন্যতম প্রধান উপায়। ২০২৫ সালে জীবন বীমার বাজার আরও উন্নত হয়েছে, এবং এখন অনেক কোম্পানি আরও নমনীয়, প্রযুক্তি-সমৃদ্ধ এবং পরিবারবান্ধব পরিকল্পনা দিচ্ছে। আসুন জেনে নিই পরিবারের জন্য সেরা জীবন বীমা পরিকল্পনা বাছাই করার গাইডলাইন ও শীর্ষ পরামর্শগুলো।

পরিবারের জীবন বীমা পরিকল্পনায় যা থাকা উচিত

| বৈশিষ্ট্য | কেন গুরুত্বপূর্ণ |

|---|---|

| যথেষ্ট অর্থ / কভারেজ | মৃত্যু বা অক্ষমতার পর পরিবারের খরচ, দেনা, শিক্ষার ব্যয় নির্বাহের জন্য যথেষ্ট পরিমাণ কভারেজ জরুরি। |

| দীর্ঘ মেয়াদি বা কনভার্টেবল অপশন | সন্তানের স্বাবলম্বী হওয়া পর্যন্ত সুরক্ষা রাখা দরকার। কনভার্টেবল অপশন থাকলে ভবিষ্যতে স্থায়ী বীমায় রূপান্তর করা যায়। |

| দুর্ঘটনা মৃত্যু ও অক্ষমতা রাইডার | অপ্রত্যাশিত দুর্ঘটনায় বাড়তি আর্থিক সহায়তা দেয়। |

| ক্রিটিক্যাল ইলনেস কভার | বড় ধরনের অসুখের চিকিৎসা খরচ মেটাতে আর্থিক সুরক্ষা দেয়। |

| প্রিমিয়াম ওয়েভার সুবিধা | অসুস্থতা বা অক্ষমতায় প্রিমিয়াম দিতে না পারলেও বীমা চালু থাকে। |

| সুবিধাজনক পেমেন্ট ও কভার বাড়ানোর সুযোগ | পরিবারের আয়-ব্যয়ের পরিবর্তন অনুযায়ী কভার বা প্রিমিয়াম বাড়ানো-কমানো যায়। |

| বিশ্বস্ত কোম্পানি ও ক্লেইম সেটেলমেন্ট রেশিও ভালো | সর্বোপরি বীমা দাবি সহজে মেটানো অত্যন্ত জরুরি। |

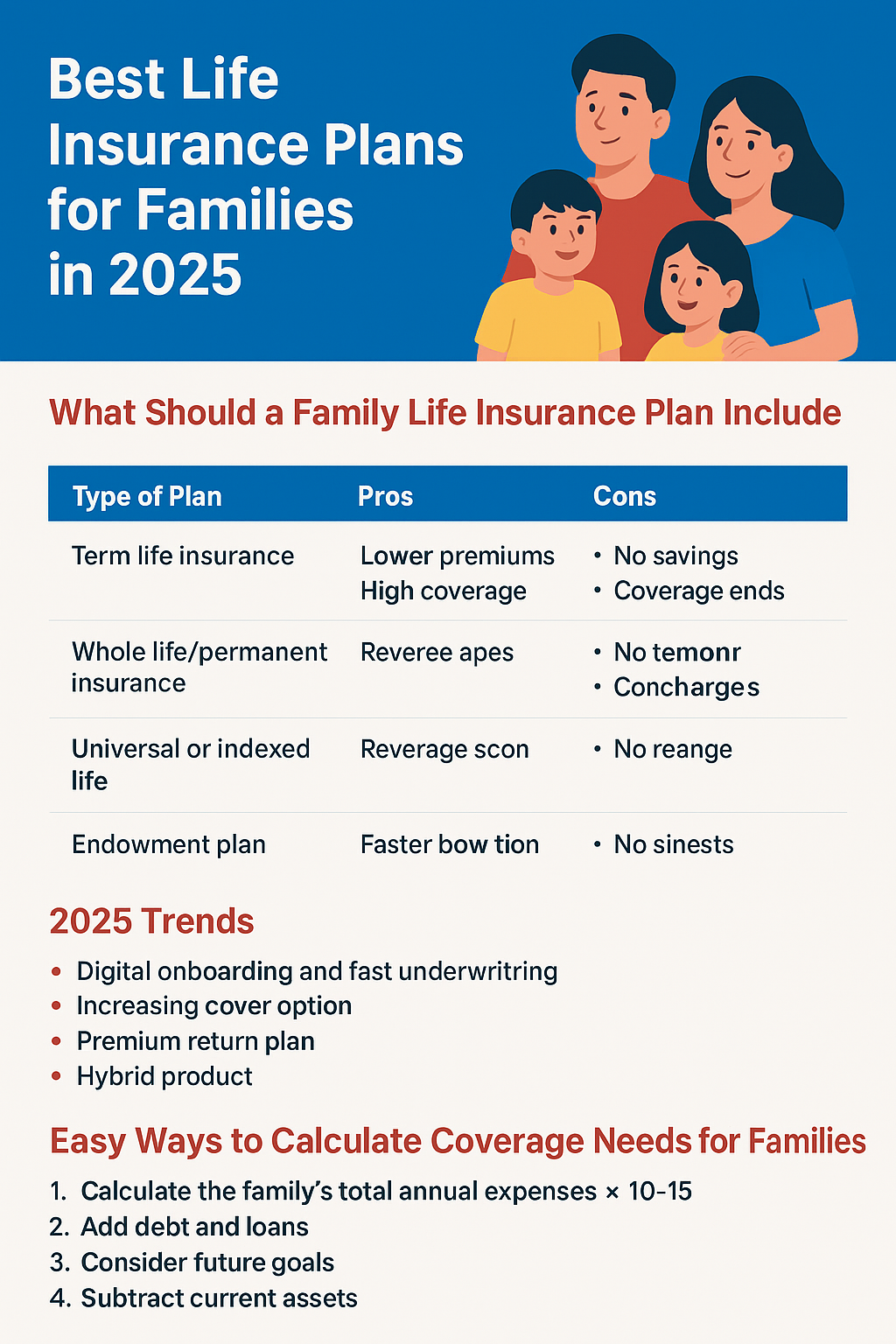

পরিবারের জন্য জনপ্রিয় জীবন বীমার ধরন

| পরিকল্পনার ধরন | সুবিধা | অসুবিধা |

|---|---|---|

| টার্ম লাইফ ইন্স্যুরেন্স | কম খরচে বেশি কভারেজ, সহজবোধ্য। | মেয়াদ শেষ হলে কভারেজ শেষ হয়। |

| হোল লাইফ / স্থায়ী বীমা | সারা জীবনের কভারেজ ও ক্যাশ ভ্যালু তৈরি করে। | প্রিমিয়াম বেশি এবং জটিল। |

| ইউনিভার্সাল বা ইনডেক্সড লাইফ | প্রিমিয়াম নমনীয়, বিনিয়োগের সুযোগ। | বিনিয়োগ ঝুঁকি থাকে, মনিটর করতে হয়। |

| এন্ডাওমেন্ট প্ল্যান | সঞ্চয় ও সুরক্ষা একসাথে দেয়। | রিটার্ন কম, খরচ বেশি। |

২০২৫ সালের নতুন ট্রেন্ড

ডিজিটাল অনবোর্ডিং ও দ্রুত আন্ডাররাইটিং – এখন অনলাইনে সহজে বীমা কেনা যায়।

ইনক্রিজিং কভার অপশন – সময়ের সাথে কভার বাড়ানো যায় যাতে মুদ্রাস্ফীতির সাথে তাল মেলে।

প্রিমিয়াম রিটার্ন প্ল্যান – মেয়াদ শেষ হলে প্রিমিয়াম ফেরত দেয় এমন প্ল্যান জনপ্রিয় হচ্ছে।

হাইব্রিড প্রোডাক্ট – মৃত্যু, অসুস্থতা ও দুর্ঘটনা কভার একসাথে দিচ্ছে।

পরিবারের জন্য কভারেজ হিসাব করার সহজ উপায়

পরিবারের মোট বার্ষিক খরচ × ১০-১৫ – মৃত্যুর পর পরিবারের অন্তত ১০-১৫ বছরের খরচ মেটাতে হবে।

দেনা ও ঋণ যোগ করুন – হাউস লোন, ব্যক্তিগত ঋণ ইত্যাদি কভারেজের মধ্যে রাখুন।

ভবিষ্যতের লক্ষ্য – সন্তানের পড়াশোনা, বিয়ে ইত্যাদির জন্য অতিরিক্ত ফান্ড ধরুন।

বর্তমান সম্পদ বাদ দিন – সঞ্চয় বা বিনিয়োগ থাকলে তা বাদ দিয়ে আসল কভারেজ নির্ধারণ করুন।

ভুলগুলো এড়িয়ে চলুন

কম কভারেজ নেওয়া।

মুদ্রাস্ফীতি বিবেচনা না করা।

সস্তা প্ল্যান নিয়ে প্রয়োজনীয় রাইডার বাদ দেওয়া।

প্রিমিয়াম নিয়মিত না দিয়ে পলিসি ল্যাপ্স করানো।

কোম্পানির ক্লেইম রেশিও না দেখে সিদ্ধান্ত নেওয়া।

উপসংহার

পরিবারের জন্য সেরা জীবন বীমা পরিকল্পনা হলো যেটি পর্যাপ্ত কভার দেয়, নমনীয়, রোগ ও দুর্ঘটনার ঝুঁকিও কাভার করে এবং একটি নির্ভরযোগ্য কোম্পানি থেকে নেওয়া হয়। বীমা শুধু একটি আর্থিক পণ্য নয়, এটি পরিবারের নিরাপত্তার প্রতিশ্রুতি। তাই বুদ্ধিমানের মতো গবেষণা করে সঠিক পরিকল্পনা বেছে নিন।

What a Good Family Life Insurance Plan Must Do in 2025

First, before you pick a plan, some key criteria to consider. The market in 2025 has been evolving—insurers are more competitive, riders more flexible, technology playing a bigger role. So these are must-haves:

| Feature | Why It Matters for Families |

|---|---|

| Adequate Sum Assured / Coverage | Enough to support dependents, cover debts, schooling, house, future obligations. Under-insurance is as bad as no insurance. |

| Long Term or Convertible Term Options | You may want coverage that lasts until children become independent / mortgage ends. Plans that allow you to convert term to permanent are useful. |

| Accidental Death / Disability Riders | These give extra financial protection if something unexpected happens. Higher usage in family plans. |

| Critical Illness / Terminal Illness Cover | Medical costs are rising. If you get critically ill, these riders help more than just death benefit. |

| Premium Waiver on Disability or Critical Illness | If the policyholder becomes disabled/ill and can’t pay, the waiver keeps the cover alive without premium payments. |

| Flexibility (Premium Payment, Policy Term, Sum Increasing) | Families go through changes—having flexibility helps. E.g., increasing cover with inflation / rising cost of living. |

| Good Claim Settlement Ratio & Reputation | Ultimately, what matters is whether insurer pays claims reliably. Customer service, transparency, financial strength are key. |

| Technology & Ease (Online Purchase / Claim Processing, Digital Tools) | Less friction, easier to manage via apps/web portals, quicker underwriting options. |

| Cost Efficiency | Lower costs per unit of benefit, minimal hidden charges, reasonable riders. |

Types of Plans & When They Suit Families

Here are types of life insurance, with pros & cons, especially for families.

| Plan Type | Advantages | Disadvantages / Considerations |

|---|---|---|

| Term Life Insurance (Pure Protection) | Cheapest large coverage, clear benefits, simple, good for dependents and major financial obligations (mortgage, children’s education). | No cash value; ends at term expiry unless converted; if you stop paying, cover ceases. Need to renew or ensure long enough term. |

| Whole Life / Permanent Life | Covers for whole life; builds cash value; some allow loans; good for lifelong dependents, estate planning. | Much higher premiums; complexity; lower growth vs investments in some cases. |

| Universal / Variable / Indexed Universal Life | Flexibility in premiums, potential investment upside; can adjust coverage amounts. | Investment risk; fees; complexity; must monitor performance. |

| Endowment / Participating Plans | Combine savings + protection; maturity benefit. For those who want forced savings. | Often lower returns, higher costs; less pure protection; the savings portion may underperform other options. |

| Whole Life with Riders | Enhances coverage (criticals, accidental, etc.) | Adds cost; need to evaluate whether you’ll use the riders. Sometimes better to buy separate insurance. |

What’s New / Trends in 2025

What’s changed lately that families should watch:

Longer maximum terms / whole life up to older ages — More insurers are offering cover up to 85‐100 years. Good for folks wanting lifelong security. Forbes+2Rupee Shastra+2

More critical illness / terminal illness riders built-in or optional — Families are expecting protection not just for death, but for illness that can drain finances. Forbes+2Suntiros+2

Better flexibility and digital onboarding — Buying online, faster underwriting, flexible payment modes. Makes things easier for busy families. Suntiros+2Campus Bee+2

Return of Premium & Increasing Sum Assured options — Some plans offer premium refunds if no claim is made, or covers that increase over time to cope with inflation. Rupee Shastra+1

Tax / Regulatory changes — In some countries, tax exemptions or changes in GST/VAT rules are affecting premiums. The Economic Times+1

Examples of Good Life Insurance Plans in 2025 (By Region)

Here are some well-rated plans that stand out. Adjust values/premiums for your country when comparing.

India

Max Life Smart Secure Plus — Offers critical illness cover, accident cover, two death benefit options. Good for families wanting robust coverage. Suntiros+2Forbes+2

HDFC Life Click 2 Protect (Super / 3D Plus etc.) — Very flexible, multiple variants, option to increase coverage, etc. Suntiros+2Rupee Shastra+2

ICICI Prudential iProtect Smart — Many critical illnesses, optional riders, good settlement ratio. Rupee Shastra+2Suntiros+2

LIC Tech Term Plan — Trusted name, straightforward, good for those wanting lower risk and high reliability. Suntiros+2Bishal Blog+2

SBI Life eShield Next — Has variants, whole life up to older ages, terminal illness benefit. Forbes+2Suntiros+2

USA / Other Markets

Pacific Life – PL Promise Term — Good for low rates + many options. Forbes

Northwestern Mutual — Excellent for whole life / permanent policies, strong reputation. Campus Bee+1

MassMutual, Guardian, New York Life — Strong players in building cash value, offering permanent cover with riders. investmentideas101.com+1

How Much Coverage Should a Family Get?

Here’s a simple method to estimate:

Calculate Dependents’ Needs — How many dependents (kids, spouse, aging parents)? What are their current and future expenses (housing, schooling, daily living)?

Debts & Liabilities — Mortgage, loans, credit card debts. If you die, these shouldn’t burden your family.

Replace Income — How many years of your income would they need if you’re no longer around? Common rule of thumb is 5-10x your annual income (but this depends on other savings and lifestyle).

Future Expenses & Inflation — Factor in higher costs of education, inflation. Also consider rising healthcare costs.

Existing Assets / Insurance — Subtract what savings, investments, retirement funds, or spouse’s income will cover. What remains is what your life insurance should aim to cover.

Mistakes Families Often Make — and How to Avoid Them

Underinsuring, because people underestimate future costs.

Not factoring in inflation / rising cost of living.

Buying cheap term plans but forgetting to add riders they might need (like critical illness, accidental death).

Letting the policy lapse due to nonpayment because they didn’t account for premium affordability in adverse situations.

Not comparing claim settlement ratio / reputation of the insurer.

Ignoring exclusions, waiting periods, small fine print.

How to Choose Your Best Plan

Decide Your Priorities — Do you want max protection at low cost? Or want something that builds cash value/investment? Or want strong riders?

Get Quotes from Multiple Insurers — Compare premium, features, riders, flexibility.

Check Financial Strength — Look up insurer’s rating (for example, AM Best, S&P, local equivalents); claim-settlement records.

Read the Fine Print — Riders, waiting periods, definition of critical illness, exclusions, process for claim.

Consider Future Flexibility — Is there option to increase cover, convert term to whole, or add on riders later?

Plan for the Worst, Hope for the Best — Ensure coverage covers worst-case scenarios (e.g., disease, disability, early death) so the family is not financially vulnerable.

Conclusion

For families, life insurance is one of the pillars of financial stability. The best plans in 2025 are those that offer sufficient coverage, flexibility, protection beyond just death (illness, accident), and good insurer reliability. While you might pay a bit more for more features or flexibility, the peace‐of‐mind is often worth it.